Insurance policies are definitely the worst way to save tax. They have consistently ranked lowest. However, though insurance plans give very low returns of 4-5%, they also inculcate a saving discipline that is so essential for building long-term wealth. Policyholders diligently pay the premium for 20-25 years to keep their policies in force and reap a huge corpus on maturity. It's no surprise then that insurance policies have helped people build property, pay for their children's education and marriage and live comfortably in retirement.

In contrast, ELSS funds have given terrific returns in recent years, but very few investors stay put for the long term. Amfi data shows that almost 35% of investments in equity funds by small investors are redeemed within a year. Another 17% are redeemed within two years, and only 48% are held for more than two years. So, while ELSS funds can give very good returns, they will not make wealth for you if you plan to exit after the three-year lock-in.

Equities had a terrific 2017, and the rally has continued into the new year. The average ELSS fund rose 36% during 2017, and even the long-term performance is fairly decent. The category has given 18% compounded returns in the past five years. Investors have seen their wealth double in a little over four years. What's more, the returns are tax free because long-term capital gains from equity funds are exempt from tax.

ELSS are still better than Ulips despite LTCG tax

While ELSS funds look attractive, the elephant in the room is the all-time high level of the market. The Nifty is trading at a PE of almost 27 and many analysts have advised investors to be cautious. Others say that expectations of returns from equities need to be toned down. Given the high levels of the markets right now, don't expect equity funds to repeat the performance of the past 1-2 years in 2018.

Some investors have stopped their SIPs in ELSS funds because markets are high. "I will restart SIPs when markets correct," says Mumbai-based Abhishek Tewari. We believe stopping SIPs for a few months will not make a significant difference to his overall returns. Tewari should continue his SIPs regardless of market levels.

An aggressive investor should invest in ELSS funds to save tax. But invest through SIPs of Rs 5,000 per month.

Smart tip: Avoid investing large sums in ELSS at one go. Take the SIP route for best results.

At the same time, investors like Vinayak should avoid putting a large amount in ELSS at one go. He needs to invest Rs 1.16 lakh in taxsaving options this week and putting the entire sum in ELSS funds at one go can be risky. Ideally, he should stagger his investments over the next 2-3 months. But he does not have the luxury of time and should, therefore, opt for some other tax-saving option this year instead of ELSS. Here are a few other things that ELSS investors should keep in mind.

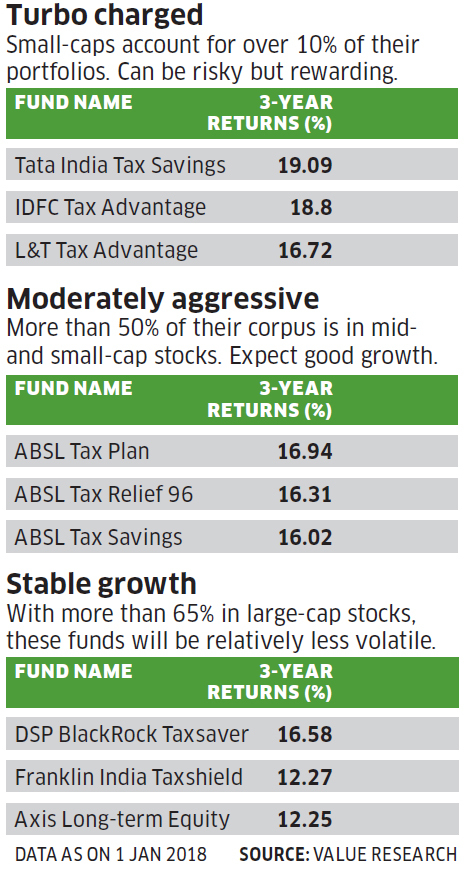

Though they offer the same tax benefits, not all ELSS funds are the same. Some are more adventurous and invest a larger portion of their corpus in small- and midcap stocks. This can be risky in the short and medium term but also rewarding in the long term. Others are relatively more conservative and line their portfolios with stable large-cap stocks. We have classified ELSS funds into three broad sub-categories (see tables). Choose the one that best suits your risk appetite.

The Best ELSS Funds

Don't base your choice on a fund's short term performance. The stability of returns is more important than the quantum of gain. Look at the 3-year and 5-year performance of the scheme before you make a choice. Small investors often treat ELSS funds as short-term investments and exit after the three-year lock in period. Look at ELSS funds as regular equity funds that should be held for the long term.

If you are investing for the long term, don't go for the dividend option. Dividends are just another way of booking profits because the amount received gets deducted from the NAV. The dividend reinvestment option is even worse. Every time the fund gives out a dividend and reinvests the money into your account, the three-year lock in period starts all over again. In effect, you are locked in for perpetuity.

2. Public Provident Fund

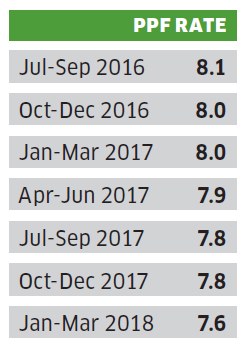

Returns: 7.6% (For Jan-March 2018)

Small savings rates are linked to the government bond yields in the secondary market. PPF rates have progressively come down in the past two years, mirroring the decline in bond yields. The PPF rate was cut recently by 20 basis points and could fall further in the coming months. Despite the rate cut, advisers say the PPF remains a good bet because the interest is tax free. The tax-free status of the PPF gives it a distinct advantage over fixed deposits. The interest from fixed deposits is fully taxable, which brings down the returns to barely 5% in the highest bracket.

PPF rates have steadily come down in past few years

On the other hand, since consumer inflation is below 4%, the PPF offers a healthy real return of more than 3%. This is quite impressive for an option that offers assured returns. Investors should continue to take advantage of this long-term tax-free product

Besides the returns and taxability, the PPF scores high on safety, flexibility and ease of investment. An account can be opened in a Post Office branch or designated branches of PSU banks. Some private banks also offer the facility to invest in the PPF. Opt for a bank that allows online access to the PPF account. Deposits can be made throughout the year, but an investor must deposit at least Rs 500 in a year.

However, there is a better alternative available to salaried taxpayers covered by the Employees' Provident Fund. Although an individual's contribution to the EPF is linked to the salary, one can opt for the Voluntary Provident Fund (VPF). The VPF offers a higher rate (8.65% for 2016-17) compared to the PPF and contributions are eligible for the same tax benefits. But this option can be exercised only at the beginning of the financial year or in October.

Smart tip: Invest through a bank that allows online access and investment in the PPF account.

Your tax-saving guide for FY 17-18

3. Senior Citizens' Saving Scheme

Returns: 8.3% (For Jan-March 2018)

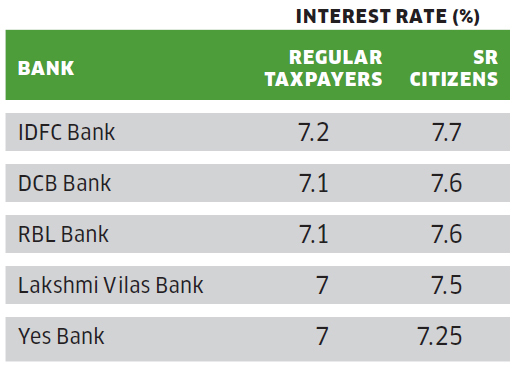

Small savings rates have been cut, but the Senior Citizens' Savings Scheme has been spared. At 8.3%, this is the best option for retirees looking for regular income in their golden years. The highest rate offered to senior citizens by banks is 7.7%. The tenure of the scheme is five years, which is extendable by another three years. However, there is a Rs 15 lakh overall investment limit per individual. Also, the scheme is open only to investors above 60. In some cases, where the investor has opted for voluntary retirement and has not taken up another job, the minimum age is relaxed to 58 years. There is also no age bar for defence personnel. There is also a clause allowing premature exits. If closed before two years, the investor has to pay 1.5% of the balance in the account. After two years, the penalty is lowered to 1% of the balance.

The Senior Citizens' Saving Scheme is a good option for retirees looking for regular and assured income in their golden years.

Smart tip: Stagger investments across several financial years to create a ladder of deposits and optimise tax benefits.

4. Sukanya Samriddhi Yojana

Returns 8.1% (For Jan-March 2018)

For taxpayers with a daughter below 10 years, the Sukanya Samriddhi Yojana is a good way to save. Although the interest rate has been reduced to 8.1%, it is still higher than what the PPF offers. Just like the PPF, the interest earned is tax free and there is an annual cap of Rs 1.5 lakh on the investment. Accounts can be opened in any post office or designated banks with a minimum investment of Rs 1,000. A parent can open an account for a maximum of two daughters, but the combined investment in the two accounts cannot exceed Rs 1.5 lakh in a year.

Some experts argue that the debt-based Sukanya scheme is not the best way to save for a long-term goal. This is true, because equity-based options can deliver higher returns. This is why experts advise that the SSY should be used in combination with other investments, such as equity funds, for saving for a child's future goals. The good part is that the girl child tag lends a sense of purpose to the investment. The maturity proceeds of other investments are often squandered. On the other hand, the Sukanya scheme helps a family save the daughter's education and marriage.

The scheme offers higher returns than PPF.

Smart tip: Open a Sukanya account in a nationalised bank to make it easier to transfer to the child.

5. National Pension Scheme

Returns: 9.5% (Past three years)

The NPS can help save tax under three different sections. Firstly, contributions of up to Rs 1.5 lakh can be claimed as a deduction under the overall Sec 80C. Secondly, there is an additional deduction of up to Rs 50,000 under Sec 80CCD(1b). Thirdly, if the employer puts up to 10% of the basic salary of the individual in the NPS, that amount will not be taxable.

The trinity of tax benefits has attracted a lot of investors to the pension scheme. However, many are still put off by the fact that NPS is not completely tax free. Only 40% of the corpus is tax free on maturity. Also, on maturity, the NPS forces the investor to put 40% of the corpus in an annuity to earn a monthly pension. This pension is treated as income and is fully taxable.

For young investors like Vinayak, the long lock-in period is also a deal breaker. NPS investments cannot be withdrawn before retirement, except in some exceptional circumstances and for specific needs. However, experts say the long lock-in period is a blessing in disguise. "When the purpose is to save for old age, it is necessary to discourage early withdrawals," says Kulin Patel, Head of Retirement, South Asia, Willis Towers Watson.

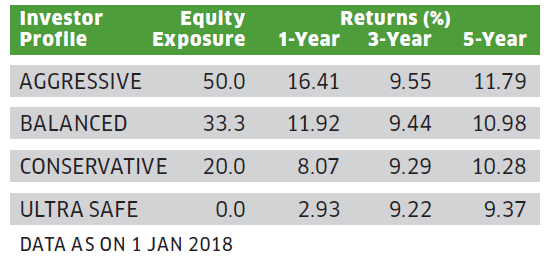

The twin rallies in equities and bonds have helped the NPS churn out good returns in the past few years. Aggressive investors who put the maximum 50% in equity funds have earned the highest returns. But this performance may not sustain in the coming months. NPS funds have lined their portfolios with long-term bonds which have not given good returns in recent months. And equity markets are looking overvalued. Even so, investors can expect better returns from NPS than pure debt products.

Rewarded by the markets

The stock market rally has boosted returns of aggressive investors who bet on equities

Smart tip: Don't be too conservative when investing for the long term. A balanced exposure to all categories works best.

Your tax-saving guide for FY17-18

6. ULIPs

Returns: 9.9-11.9% (Past five years)

Despite attempts by distributors and insurance companies, the perception about Ulips has not changed much. Investors still consider them very costly and financial advisers continue to hold them in contempt. But it is time to bury the shady past of Ulips. New Ulips launched by insurance companies are low on costs, which translates into better returns for investors.

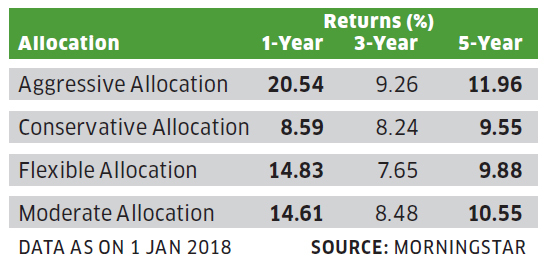

Morningstar data shows that aggressive Ulip plans earned over 20% in the past one year. That may not appear impressive compared to the 30-35% that equity mutual funds earned for investors. The 11.96% returns from Ulips in the past five years are not even a patch on what equity funds have earned since 2012. Besides, some of the charges of the Ulip are not deducted from the NAV so the actual returns for the investors may be even lower.

But Ulips have one distinct advantage over mutual funds. Switching from equity to debt or vice versa does not have any tax implications. Being insurance policies, the income and capital gains from these plans is tax free under Section 10(10D). This makes a Ulip a convenient rebalancing tool for investors who reset their portfolio's asset allocation every year.

They will also be useful for investors wanting to put money in debt funds but are deterred by the taxation of short-term gains. The minimum period for long-term capital gains from debt and debt-oriented funds has been increased from one year to three years. If held for less than three years, the gains are added to your income and taxed at the normal rate. But there is no tax on short-term gains from Ulips.

You can also park short-term money in the liquid fund of your Ulip using the top-up facility.

How Ulips fared

Smart tip: If investing large sum, opt for liquid or debt fund of the Ulip and gradually shift the money to equity funds.

What to see in a Ulip

CHARGES: The most important consideration. Some charges are built into the NAV while others are levied by deducting units. Look up all charges mentioned in the brochure.

FUND OPTIONS: Look at the various fund options available. There are three basic funds: equity, debt and liquid, but some insurers offer hybrid funds and other options.

SWITCHING: Know how much the Ulip will charge for switching from one option to another. Normally 3-4 switches a year are free, though some offer up to 12 free switches.

WITHDRAWALS AND TOP UPS: Find out rules relating to top up investments and withdrawals from policy.

COVER: Be sure whether your Ulip will pay only the sum assured or also the fund value in case of a mishappening. Some Ulips pay only the sum assured, though their premium is also lower.

7. NSCs

Returns: 7.6% (For Jan-March 2018)

The interest rate of the NSCs has been reduced to 7.6%, but are still more than what bank fixed deposits offer. The NSCs also have a sovereign backing. NSCs fell out of favour when bank rates were higher at 9-9.5% a few years ago. But deposit rates have now fallen to 6.5-7%, though senior citizens get higher rates. This makes the NSCs more attractive than bank deposits.

What's more, the interest earned on the NSC is also eligible for deduction under Section 80C in the following years. Here's how this works. Suppose an investor buys Rs 50,000 worth of NSCs in January 2018. One year later, the investment would have earned an interest of about Rs 3,800. The investor can claim deduction for this Rs 3,800 for the year 2018-19. The next year, the investment would earn about Rs 4,100 in interest. This can be claimed as a deduction in 2019-20.

This is especially useful for investors in the 5% tax bracket who are not able to fully exhaust the Rs 1.5 lakh investment limit under Sec 80C. The tax deduction available on the interest effectively makes it tax free for such investors.

There have been some changes in the rules for non-resident Indians investing in small savings schemes lately. NRIs are no longer allowed to invest in these instruments. The PPF account of an individual will be deemed closed from the date he becomes an NRI and he would get only 4% interest from that date onwards. Similarly, NSCs will be deemed to be encashed by the holder on the day he becomes an NRI.

Smart tip: Create a ladder of NSCs so that after they mature the proceeds can be reinvested to earn benefits.

8. Pension Plans

Returns: 7-10% (For past one year)

The emergence of the NPS has pushed pension plans from insurance companies into oblivion. Unlike the new Ulips where charges have come down significantly, the pension plans from insurance companies continue to have high charges. Interestingly, these pension plans are more lenient than the NPS when it comes to deploying the maturity proceeds. NPS investors have to compulsorily put 40% of the corpus in an annuity. Some pension plans don't have such restrictions, while some others require only 25% to be put in annuities. But on the other hand, only 33% of the corpus is tax free on maturity, compared with 40% in case of the NPS.

According to a recent RBI report, the population of Indians above 65 years old is expected to grow by 75%. The report also points out that only a small fraction of this age group has saved in private pension plans and a large segment of the total population has not actively taken steps to ensure adequate financial coverage during retirement.

Insurance companies believe that the tax treatment of annuities and pension income is one of the main reasons why people don't invest in pension plans. There might be several reasons for people not saving for retirement but the taxability of pension plans is certainly one of them.

Right now, if an investor does not buy an annuity on maturity, 66% of the corpus of the pension plan is taxed. Even the pension from the annuity is treated as income and taxed accordingly. Both these tax rules should be relaxed as far as possible in the coming Budget which will give a boost to the entire pension space and encourage Indians to plan for a worry-free retirement

Smart tip: Rebalance pension plan portfolio periodically to restore original asset allocation, thus reducing risk.

9. Bank FDs

Returns: 7 to 7.7%

Their interest rates have fallen significantly and the income is fully taxable. Yet tax-saving bank fixed deposits are a good choice for the Rip Van Winkles who left their tax planning for the last minute and are now running around to beat the deadline. Vinayak has to show the proof of investment under Sec 80C by the end of this week or his company will deduct a very high tax from his January salary.

For such taxpayers, the Net banking facility is a godsend. Even if the bank branch has closed for the day, his tax planning can be done in a matter of minutes. All he has to do is open a tax-saving fixed deposit and show the proof of investment to your company.

We are suggesting bank fixed deposits for the simple reason that he cannot go wrong in these instruments. Sure, the income is taxable and the post-tax returns will be barely 5.5%. But at least Vinayak won't end up buying a low-yield life insurance policy or an unsuitable pension plan.

These fixed deposits are also suitable for senior citizens who might already have hit the Rs 15 lakh ceiling in the Senior Citizens' Saving Scheme and don't want to lock in money for the long term in a PPF account. Though NSCs offer higher rates than most banks, they still require the investor to visit the post office. Bank deposits can be done online.

Keep in mind that the interest from such deposits has to be reported in the tax return next year. Many investors have the misconception that up to Rs 10,000 earned on bank deposits is tax free. The exemption under Sec 80TTA applies to savings bank interest only. Income from fixed deposits is fully taxable and should be mentioned in the income tax return of the individual.

The best tax-saving FDs

More than 50% of their corpus is in mid and small-cap stocks. Expect good growth.

Smart tip: Opt for the quarterly or yearly interest payout option if you don't want to lock up your money for five years.

10. Insurance

Returns: 4.5-5%

It is no surprise that life insurance policies are at tenth place in our ranking of tax-saving options. Life insurance is the bulwark of a financial plan because it safeguards all the goals of the individual even if he is not around. But this purpose is best served by a pure protection term insurance plan rather than a costly traditional policy that gives back money at periodic intervals or provides a huge corpus on maturity.

Traditional policies yield barely 4-5% returns but investors are attracted to them because the agent quotes a very high maturity figure. Buyers don't realize that there is a time value of money. If an insurance policy will give Rs 40 lakh in 20 years, even 6% inflation would pare down its value to less than Rs 12 lakh.

Manoj Srinivas is not able to save for other goals because he pays a very high insurance premium for a policy that covers him for less than his annual income. He should surrender this policy or turn it into a paid up plan. This will free up Rs 1 lakh a year, which can be put to good use elsewhere. A term cover of Rs 1 crore will cost him around Rs 10,000-14,000.

He pays Rs 1 lakh premium for a cover of Rs 5 lakh, though a term plan can cover him for Rs 1 crore at a cost of only Rs 12,000-14,000 a year. The high premium outgo prevents him from investing for other goals.

Smart tip: A pure protection term insurance plan can provide a large cover at a very low cost.

SIPs are Best Investments as Stock Market s are move up and down. Volatile is your best friend in making Money and creating enormous Wealth, If you have patience and long term Investing orientation. Invest in Best SIP Mutual Funds and get good returns over a period of time. Know which are the Top SIP Funds to Invest Save Tax Get Rich - Best ELSS Funds

For more information on Top SIP Mutual Funds contact Save Tax Get Rich on 94 8300 8300

OR

You can write to us at

Invest [at] SaveTaxGetRich [dot] Com

No comments:

Post a Comment